Where the D2D Revolution Stands: Spectrum, Partnerships, and New Market Realities

The direct-to-device (D2D) satellite connectivity market has been utterly transformed by a series of disruptive multi-billion dollar deals and a new wave of global competition, heralding the arrival of universal device connectivity at a pace and scale few anticipated just months ago. This brief overview covers key insights and analysis, providing deeper industry context, technical evolution, and the strategic implications of the emerging D2D marketplace.

Universal Connectivity, Strategic Stakes, and Market Acceleration

Recent months have upended long-held assumptions about the timeline and competitive structure of D2D satellite connectivity. Once considered niche and far-future, D2D is now widely seen as a catalyst for redefining mobile network reach, enabling continuous service for billions of devices in regions inaccessible to terrestrial carriers. This shift promises not only to connect remote users and critical infrastructure but to drive new IoT, automotive, and enterprise markets, with revised forecasts sharply upward to project $15 billion in annual D2D service revenues by 2033 and user bases exceeding 400 million monthly by the same time frame.

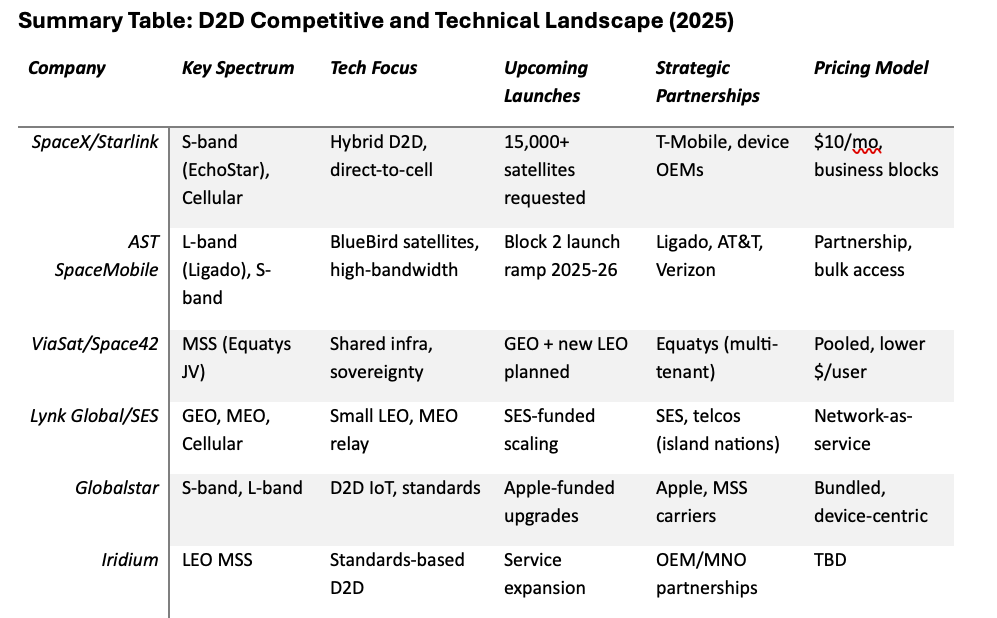

The SpaceX-EchoStar spectrum deal, a $17 billion transaction that includes multi-band S-band MSS holding, was quickly followed by spectrum consolidation moves from Viasat and Space42 (via the Equatys joint venture). These developments illustrate a shift from one-off spectrum partnerships to pooled models designed to support sovereign architectures and reduce per-user infrastructure costs, challenging the dominance of any single party and appealing both to national regulators and commercial telcos.

Business Models, Pricing, and Adoption Risks

Recent surveys suggest growing consumer willingness to pay for D2D service, with about 60% of mobile subscribers globally open to incremental fees for reliable satellite coverage, though most expect only modest price increases (typically 5-10% over baseline mobile plans). This aligns with T-Mobile and Starlink’s $10/month pricing for enhanced D2D messaging, while enterprise-focused Starlink business plans now feature high terminal access costs and data blocks ranging from $42 to $885, subject to geographical tiering. As usage grows, carriers will increasingly bundle basic emergency or messaging-oriented satellite services into existing plans, reserving premium tiers for higher-bandwidth applications.

However, aggressive throttling policies (notably Starlink’s shift to one megabit per second speeds after priority data caps are exceeded) and unclear cost management frameworks remain hurdles for business adoption and market clarity. As device makers and mobile network operators race to differentiate offerings, manufacturers will be incentivized to integrate satellite capability into new handsets at scale, spurring upgrade cycles and competitive feature launches.

Technology Development: Antenna, Spectrum, and Standardization

D2D technical progress is rapid, with improvements in phased array antennas (AST SpaceMobile’s planned Block 2 units will be over 190 square meters—more than three times previous commercial deployments), waveform design, and inter-satellite routing supporting higher bandwidth and seamless global operation. China is advancing multi-orbit D2D programs, Europe’s IRIS² project is targeting sovereign D2D networks, and Eutelsat/OneWeb are already piloting LEO broadband and D2D features in partnership with telecoms.

Importantly, the newly cleared spectrum allows SpaceX to experiment with hybrid terrestrial/satellite networks, potentially enabling a user experience akin to 5G and reducing reliance on partners such as T-Mobile. The integration of chipsets for “direct-to-cell” compatibility is underway with several major semiconductor manufacturers, supporting broader device coverage and new regulatory frameworks for hybrid multi-band handsets.

Sovereignty, Shared Infrastructure, and Geopolitical Implications

The rise of sovereignty-focused models, such as Equatys, signals a major realignment in satellite telecom: countries and regional operators are seeking to maintain influence, access, and compliance via pooled spectrum and shared infrastructure, avoiding dependency on a single vendor or network. This stands in contrast to legacy direct-to-satellite plays, which faced barriers in spectrum acquisition and interoperability.

Incidents such as Starlink’s ability to bypass national infrastructure in sanctioned markets have sharpened regulatory scrutiny, and ventures like Equatys now offer alternatives tailored to sovereign compliance and national carrier operation. Seen through the lens of policy and security, D2D is increasingly viewed as central to national communications resilience, making investment, technical choice, and vendor relationships key issues for government buyers and military end users.

Competitive Dynamics, Upcoming Launches, and Future Outlook

With over 8,000 Starlink satellites launched and 15,000 more requested by SpaceX, the industry’s capacity and ambition have entered new territory. Viasat and Space42 aim to deliver shared D2D services within three years, using both existing GEO/MSS satellites and new LEO deployments. AST SpaceMobile and Lynk Global are rapidly acquiring multi-band spectrum and scaling manufacturing - Lynk’s SES partnership provides multi-orbit resiliency and offers sovereign channel access for government, automotive, and MNO customers.

Novaspace, Globalstar, and Iridium continue pursuing standards-based service offerings, leveraging existing infrastructure for incremental D2D adoption. IoT is a particularly dynamic opportunity, with 30 million D2D IoT connections forecast by 2030, though pricing structure and airtime economics remain a constraint for broad uptake.

Industry consolidation (SES-Intelsat merger), competitive launches (Apple-funded Globalstar upgrades), and evolving business models point to continued fragmentation, but also to a maturing commercial ecosystem, where spectrum control, technical leadership, and sustainable economics will define the winners as D2D becomes standard in mobile handsets and enterprise networks.

Implications for Investors, Policymakers, and Industry Stakeholders

The D2D market in 2025 is characterized by the consolidation of spectrum, emphasis on sovereign compliance, and innovative business models, all contributing to an expected double-digit annual growth rate and increased adoption driven by device upgrades. As the industry transitions from technical demonstrations to commercial rollouts, investment flows are expected to intensify, leading to further operator consolidation and ongoing regulatory adjustments to balance emerging commercial opportunities with national interests. In the near term, companies that secure spectrum access, ensure device compatibility, and develop scalable, cost-effective infrastructure will gain a competitive edge. Looking ahead, the long-term leaders will be those who successfully integrate D2D technology into essential areas such as public safety, IoT, and emergency communications, serving both developed and developing markets.

These insights position the D2D satellite connectivity sector as one of the most dynamic spaces in global communications, marked by strategic deals, rapid technology evolution, and the reframing of connectivity as a universal right, transforming both the mobile industry and public policy worldwide.