The Account They Won’t Open

Europe is pouring record money into defense tech, and many of those same founders still can’t open a basic business bank account.

There’s a story making the rounds in defense circles that’s almost too good to be true. A Ukrainian drone manufacturer, TAF Industries, needed a simple bank loan. The bank wanted collateral, which meant the bank wanted to see the factory. But the factory’s location was a state secret: reveal it, and you’ve handed a targeting package to a Russian missile crew. So the company’s CEO did the only logical thing: he blindfolded the bank officials and drove them to the site. It worked. They got the loan.

It’s a story that compresses the entire problem into a single image. But here’s the thing: getting the loan was the hard-won part. There’s a more basic indignity sitting underneath it, one that almost never makes the headlines: across Europe, a lot of the founders Europe is counting on to rearm the continent can’t even open a business bank account. Not borrow. Not raise debt against a contract. Just open an account, get a debit card, and run payroll like any café or plumbing firm. That’s the part the funding announcements hide. And the funding announcements are loud.

The paradox: a record funding year, and founders who can’t get a debit card

In 2025, venture capital poured a record $5.2 billion into European defense, security, and resilience startups, according to the joint report from the NATO Innovation Fund and Dealroom. Helsing, the Munich headquartered defense technology company, hit an estimated $18 billion valuation in May 2026 during a $1.2 billion funding round led by Dragoneer Investment Group and Lightspeed Venture Partners, making it Germany’s most valuable startup, full stop. On June 9th, Finland’s ICEYE officially announced its Series F funding round at a $12 billion valuation. Quantum Systems, also German, cleared $3.5 billion. Portugal’s Tekever crossed a billion dollars. If you only read the funding announcements, you’d think European defense tech had never had it so good. But equity is not the same thing as banking. And underneath the mega-rounds, the most boring piece of financial plumbing, the current account, is broken.

At a Munich Security Conference panel hosted by Resilience Media, investors described startups in Ukraine and Germany having to register, in effect, as “drone companies used to deliver fertilizer to Russia” just to get an account opened, because the word “defense” trips every alarm in a bank’s onboarding system. The detail that should stop you cold: even the NATO Innovation Fund itself struggled to open a bank account. When a fund explicitly created by the NATO alliance can’t clear an onboarding check, the problem isn’t the founder. It’s the system.

This is the part founders find genuinely surreal. They’ve closed a round. They have term sheets, a board, a government customer, and a local bank still won’t give them an account, or quietly off-boards the one they have. An account refusal isn’t a financing inconvenience; it’s an existential one. You can’t receive a government payment, run payroll, or pay a supplier without somewhere to put the money. A startup can survive a “no” on a loan. It cannot operate without an account.

And then, yes, there’s the second-order problem: credit. Sandra Golbreich, a general partner at Vilnius-based BSV Ventures, where roughly half the portfolio is defense-related, put a number on it to Defence Nordic: even a startup holding a long-term contract with a defense ministry or a prime contractor has, by her estimate, about a 10% chance of getting a bank loan. She described a dual-use company in her own portfolio that was turned away by a major Nordic bank despite holding contracts with several governments. Her diagnosis is blunt: the banks “are still using the same criteria, looking at cash flow and balance sheets,” and a defense startup simply doesn’t look like that.

Why a “good problem” is actually a fatal one

You might reasonably ask: if the VC money is there, who cares about a bank account or a loan? Founders care, because banking and equity do different jobs, and the jobs banking does (holding the money, moving the money, bridging the gap between contracts) are exactly the ones a defense startup can’t skip.

Defense revenue arrives lumpy and late. You win a big government order, you ship, and then you wait, frequently 60 days or more, to get paid. In between, you have to make payroll, buy components (often cheaper in bulk, often from abroad), and bridge to the next procurement contract. That’s textbook working capital, the most ordinary thing a bank does for any other business on earth. Serhii Goncharov, who heads Ukraine’s National Association for Defense Industries, describes precisely this: companies need credit “to smooth production during gaps between big government procurement contracts.” Without it, a startup with a full order book can still die of thirst.

The knock-on effect distorts the whole capital stack. Because founders can’t borrow against their first signed contract, they’re forced to raise enormous seed and Series A rounds, with correspondingly large valuations and dilution, simply to buy enough runway to prototype and scale. That’s the “valley of death” for hardware: the brutal stretch between a working prototype and volume production, where capital requirements are highest and financing is thinnest. Equity is the most expensive money in the world to fund a 60-day receivable with. Yet that’s exactly what these companies are being asked to do.

Why banks actually say no (it’s not what you think)

It’s tempting to blame squeamish bankers who don’t like weapons. The real answer is more bureaucratic and, in a way, more frustrating: most of the “no” comes from compliance machinery and reputational risk, not a considered judgment about the company.

Several forces stack up. First, AML and KYC, the account-killer. Defense touches export controls, end-user restrictions, classified work, and opaque supply chains. To an automated onboarding system, that reads as risk, full stop. The same machinery built to catch money launderers flags a legitimate drone startup at the account-opening stage and never lets a human look closer. This is why account refusal, not loan refusal, is the first wall founders hit.

Second, ESG and reputational fear. For most of the last decade, defense sat in a “grey zone” where it was treated as ESG-incompatible almost by default. As the Bruegel think tank argued, the EU’s sustainable finance rules don’t actually prohibit lending to defense, but the fear of looking un-green does the blocking just as effectively. The data backs this up: as of early 2024, only around 30% of EU and UK investment funds had any exposure to aerospace and defense at all (versus roughly 37% in the US), per the Principles for Responsible Investment. Most defense equipment isn’t labelled “green” under the EU taxonomy unless it’s explicitly dual-use, so it falls through the cracks of the very framework that’s supposed to direct capital.

Third, outdated risk models. Golbreich points to Europe’s structurally risk-averse approach to capital, much of it hardened by post-2008 banking regulation. The models reward tangible collateral and diversified, predictable cash flow. A defense startup that rents its office, sells mostly to one government customer, and keeps its locations secret fails every box, even when its order book is enormous. The Ukrainian case makes it almost literal: banks want to lend against buildings and machines; young defense firms have turnover, not real estate, plus the unique wartime risk that a missile erases the collateral overnight.

And fourth, the one that’s coming rather than going: the capital rules themselves. Deutsche Bank’s chief risk officer, Marcus Chromik, has warned that the incoming Basel 3.1 regime is already restricting financing for the smaller companies in Europe’s defense supply chain, because firms without an external credit rating force their lenders to hold more capital against the loan. His line at a Frankfurt banking conference was darkly memorable: he didn’t want it on the industry’s tombstone that “they didn’t have tanks, but the banking regulation was really fair.” When the risk chief of Germany’s biggest bank is sounding this alarm, the problem isn’t a few jumpy onboarding clerks. It’s structural.

The hole where the startup bank used to be

There’s a ghost hanging over all of this, and its name is Silicon Valley Bank. Before March 2023, SVB was the bank that understood startups, the one institution genuinely comfortable lending against venture backing and intangible assets instead of buildings and machines. When it collapsed, founders on both sides of the Atlantic suddenly discovered how few banks were willing to do that work. In Europe, regulators moved fast to stop the bleeding: SVB’s UK arm was sold to HSBC for a nominal £1, depositors were protected at zero taxpayer cost, and the unit carried on as HSBC Innovation Banking. Germany’s BaFin briefly froze SVB’s Frankfurt lending branch before allowing it to resume.

So the lights stayed on. But for defense founders specifically, the rescue carried a sting. The most startup-fluent balance sheet in Europe got folded into HSBC, a bank that has historically maintained activist sustainability policies excluding weapons. The institution most willing to take a flyer on a hard-tech founder is now inside one of the institutions most likely to say “not defense.” The net effect of the SVB era is that Europe lost its specialist startup bank and gained more concentration in exactly the kind of large, compliance-cautious lender that struggles with this sector. The lesson founders actually absorbed was narrower and sharper: never depend on a single banking relationship, because the friendly one can vanish overnight.

The map is wildly uneven: where Europe says yes, and where it says no

Here’s where it gets interesting for anyone actually choosing where to build. Europe is not one market for this. The banking experience for a defense founder varies enormously by country, and the variation tracks two things: how close the country sits to the threat, and how its banking culture is wired. (A third axis cuts across all of them, and it matters just as much: a proven scale-up raising a syndicated nine-figure package is now a very different animal from a seed-stage founder trying to open a first account.)

The supportive end: the Baltics and the Nordics. When Russia is across your border, “defense” stops being controversial and becomes existential. Estonia, Latvia, and Lithuania have all committed to spending 5% of GDP on defense by 2026, a decade ahead of most of NATO, and they’ve built financing scaffolding to match. Latvia’s Defence Industry and Innovation Support Strategy, adopted in March 2025, ramps defense-innovation funding toward 3% of the budget by 2036, mandates a rising share of local suppliers, and stands up a dedicated Defense Innovation Fund to build homegrown startups. Lithuania drew a €400 million defense loan from the Nordic Investment Bank and signed a €300 million EIB credit line tagged to the EU’s new SAFE instrument. The regional banking culture helps too: the Baltics opened their banking sectors to foreign (largely Nordic) ownership years ago, and they’re among Europe’s most fintech-forward, digitally-native financial markets.

France: the activist-state model. France has decided that financing defense is a sovereignty issue and is acting like it. Bpifrance, the state investment bank, runs a dedicated defense-SME financing program (Def’fi) and a defense-tech equity vehicle (Definvest). In November 2025 it issued the first “European Defence Bond“: €1 billion, nearly four times oversubscribed, with two-thirds of the allocation going to investors outside France. The BPCE banking group did a €750 million defense bond before that. Luxembourg followed with sovereign defense bonds that are income-tax-exempt for residents. When the state signals this loudly that defense finance is legitimate and patriotic, commercial appetite follows.

Germany: improving at the top, brutal at the bottom. Germany is the most interesting case, because the easy story, “German banks won’t touch defense,” is now only half true, and the false half matters. At the scale-up end, the picture has flipped fast. In February 2026, drone-maker Quantum Systems closed a €150 million long-term debt package from the EIB, Commerzbank, Deutsche Bank and KfW, with Commerzbank noting it had been the company’s house bank since its early growth phase. The state development bank KfW now runs a Venture Tech Growth Financing program and, via the new Deutschlandfonds, channels capital into deeptech, cybersecurity and defense, with direct co-investments reported up to €50 million. Germany’s Zeitenwende has genuinely moved the big corporate desks and the public banks; BNP Paribas, further afield, even loosened its own “controversial weapons” policy to keep pace.

The problem is that none of that reaches a two-person seed-stage team. The friction in Germany is concentrated exactly where the headlines aren’t: at early-stage onboarding, at the consumer-grade fintechs, and behind a thicket of genuine legal guardrails. The “debanking” reflex is real: the Sparkassen, the largest banking group in Europe by assets, run a conservative, collateral-heavy model that is almost the opposite of what a pre-revenue startup needs. On top of that sits real law: as Ashurst’s analysts note, a constitutional prohibition on stockpiling war weapons plus a permit requirement for production outside specific government tenders puts a ceiling on how an early-stage drone company can scale. Add foreign-investment screening (a notification trigger once an outside investor crosses 10% of voting rights in export-controlled tech) and BAFA export-compliance demands, and a bank’s legal team scrutinizes every transaction. So Helsing and Quantum Systems land syndicated nine-figure packages while the seed-stage founder still can’t open a current account. The German divide isn’t really country-versus-country anymore; it’s scale-up-versus-startup, and corporate-desk-versus-app.

The neobank trap: the apps can’t tell a radar company from a missile company

A natural instinct is to route around the dinosaurs and go digital. It’s the wrong instinct: the retail fintechs are, if anything, the worst offenders, and understanding why exposes the core absurdity of the whole system.

At a real bank with a human compliance team, “defense” isn’t one undifferentiated blob. Counter-UAS, the business of stopping hostile drones, is the cleanest illustration. If your startup builds the soft-kill side (radar, RF sensors, AI threat-detection, signal jamming), you sit squarely in dual-use territory, and banks actually like that, because the same kit protects airports, prisons, power plants and stadiums. The friction spikes only at the hard-kill end (interceptor drones, net-guns, anything kinetic), which trips the legacy ESG filters and months of enhanced due diligence. A competent banker can tell those two profiles apart and price them differently.

A neobank’s algorithm cannot. Its compliance is automated keyword-matching at scale, and “defense,” “military,” or “drone” is the flag, so the passive-radar company and the missile company get the identical instant rejection. Revolut Business is explicit about it: it won’t onboard “armaments, nuclear, weapons or defense manufacturers,” and refuses anything tied to the UK’s strategic export-control lists, in every country it operates. (That Revolut was co-founded by a man of Ukrainian heritage is an irony no one in this world misses.) Wise is the same story, and arguably starker: its Acceptable Use Policy restricts “weaponry, military and semi-military goods and services,” and spells out that this includes “military software, or any other goods or services intended for military use.” Read that twice. Military software. A pure-software, passive C-UAS startup that never goes near a munition is still out, and founders report rapid account closures the moment a defense transaction or an investor wire lands. (One disambiguation, because the name trips people up: “Wise” in European defense circles usually means Startup Wise Guys, the Tallinn accelerator that actively backs defense and cyber founders, the exact opposite posture to the fintech.)

Two nuances matter here, though. The first: this is a consumer-neobank problem, not a digital-banking problem. The mass-market apps run the identical model (an algorithm protecting a retail license across millions of users, with no human to read your export paperwork), and they’re uniformly hostile: what’s true of Revolut and Wise is true of N26, Bunq and Monzo. But a separate breed of corporate digital bank underwrites manually and will bank dual-use and defense. Founders have more luck with B2B institutions like Lithuania’s EMBank and Aion Bank, or Estonia’s tech-forward LHV, especially once a regional defense hub or an EU grant has already validated them. France’s Qonto sits in between, more open to software-defined defense and cyber than the consumer apps, though it still scrutinizes anything kinetic. So the rule isn’t “avoid digital banks”; it’s “avoid consumer apps, and bank somewhere a human signs off.”

The second: even among the consumer apps, Revolut is increasingly the outlier rather than the rule. As The Banker notes, it’s among a shrinking minority of European lenders keeping a blanket defense exclusion while traditional and institutional banks move the other way; BNP Paribas, for one, loosened its own “controversial weapons” policy to keep pace. The honest takeaway is blunt: never run a defense company’s core banking on a mass-market app that might wake up and decide it doesn’t like you. Keep any fintech as a secondary rail at most.

Who’s starting to say yes (and why)

For years the honest answer to “which big European bank will take a defense startup?” was “almost none.” That is shifting, and the lever is the European Investment Bank.

In June 2025 the EIB tripled its Pan-European Security and Defence Lending Envelope to €3 billion and signed its first commercial-bank deal under the scheme with Deutsche Bank: a €500 million EIB loan that lets Deutsche on-lend €1 billion in financing and working capital to SMEs across the EU defense supply chain. The mechanism matters more than the number. By providing intermediated loans and guarantees, the EIB absorbs a chunk of the risk that made commercial banks flinch, and demand was strong enough to force the threefold increase. Santander soon followed with an EIB-backed facility to unlock roughly €900 million for security, defense and other strategic sectors. The one-stop “Security and Defence Office“ the EIB has stood up is now the closest thing Europe has to a front door.

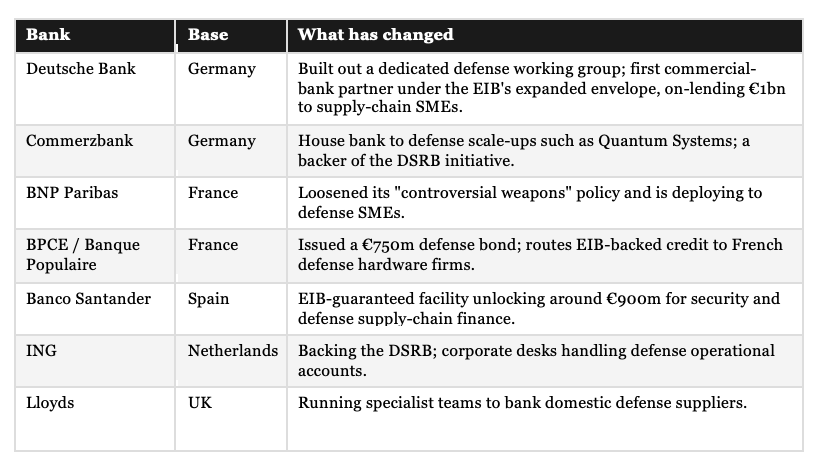

That is pulling the big commercial banks back in, and several have built dedicated defense coverage:

One caveat, stated plainly: several of these same institutions were debanking defense firms barely a year earlier. In 2024, Santander and Lloyds were named before the UK Treasury Committee for closing roughly 300 “public administration and defense” accounts between them. The welcome is real but new, partial, and concentrated in the corporate and investment-banking desks; the retail arms and automated onboarding flows have not necessarily caught up. That is precisely why, as a founder, the channel you use to approach a bank matters as much as which bank it is.

The American answer: a defense founder builds his own bank

Here’s the most telling response to this whole mess, and it came from the United States. If no existing bank will serve hard-tech and defense founders, why not charter a new one?

That’s Erebor. Founded in 2025 by Anduril co-founder Palmer Luckey and Palantir co-founder Joe Lonsdale (with backing from Peter Thiel’s Founders Fund, Lux Capital, a16z and others), Erebor won a full national bank charter in early February 2026, the first new US national bank chartered under the second Trump administration, and opened for business out of Columbus, Ohio with roughly $635 million in capital and a valuation around $4 billion. Its explicit purpose: serve the slice of the innovation economy that traditional banks avoid (AI, crypto, advanced manufacturing, and defense), precisely the gap left when SVB collapsed. Luckey, whose own Anduril had banked with SVB, calls it “a farmers’ bank for technology.” Columbus is no accident either; Anduril is building its Arsenal-1 megafactory in the region.

The symbolism is hard to miss. The banking system was so unwilling to serve defense founders that one of the world’s most prominent defense founders went and built a bank. It’s not been frictionless: Senator Elizabeth Warren has questioned the speed of the approval and the risk profile. But the charter is real and the doors are open.

The catch, for European readers, is that none of this fixes Europe. Erebor is a US-chartered bank serving US clients. A drone startup in Vilnius or Munich can’t bank there. But it’s instructive in two ways. First, it proves the demand is real and bankable enough that serious capital will charter an institution around it. Second, it sharpens a contrast worth sitting with. America’s answer to debanked founders was up and running in under a year: a private bank, chartered and open for business. Europe’s most ambitious answer, the multilateral defense bank described below, is far bigger in scope but won’t be formally established until the end of 2026, and it’s aimed at sovereigns and supply chains, not at opening a seed-stage startup’s current account. The continent actually on the front line is moving on a longer clock.

What founders can actually do right now

None of this is reason to give up; it’s reason to be deliberate. If you’re building in this space, a few moves genuinely change your odds.

Lead with the dual-use framing wherever it’s honest, because dual-use is the category that the taxonomy, the ESG funds, and the cautious banks can all say yes to. Choose where you domicile and bank with the same care you’d choose a co-founder: the Baltics and France will meet you halfway in a way Germany’s high street won’t, though you have to weigh that against each country’s export-control and permitting regime. Build banking redundancy from day one: the SVB lesson is that a single relationship is a single point of failure, so pair a primary operational account with a backup before you need it, and keep any neobank strictly as a secondary rail. When you do approach a commercial bank, go to a corporate or institutional desk with a real compliance team, not a mass-market app: the desks that wrote Quantum Systems’ €150 million package exist; the apps that auto-reject you are a dead end. If the high-street banks stall, specialist EU institutions built to manually underwrite the cases retail apps auto-reject, Lithuania’s EMBank among them, are worth a look. But the single most reliable way in is a warm introduction: if you’re backed by a defense-focused fund, have your investors walk you straight to a banking desk that already speaks compliance. Walk into that conversation with the paperwork that lets a compliance officer say yes: incorporation documents, a capital-deposit account ready for your share capital, your export-control classification numbers, and a one-page summary of your business model, product classification and intended end-users, with a written undertaking that you sell only to NATO or allied governments. And if you build kinetic hardware, consider structuring cleanly: keeping your software and AI work in a standalone civilian entity can let you run everyday payroll and SaaS subscriptions through ordinary business accounts while the hardware sits in a separate, defense-classified company, provided you do it transparently rather than to obscure what you are. Stack your file with institutional validation (an EDF grant, a place in the EUDIS accelerator, NATO Innovation Fund backing), because each one measurably shortens a bank’s enhanced-due-diligence process. Get onto the national promotional-bank programs built for exactly this: Bpifrance’s Def’fi in France, KfW’s Venture Tech Growth Financing and the Deutschlandfonds in Germany, SAFE-linked credit lines, and the EIB’s expanded defense perimeter. Partner with a prime contractor for market access and balance-sheet stability: Golbreich’s caveat is that you have to survive inside an organization obsessed with margins, but the access is real. And tap the specialist capital that actually understands you: defense-focused VCs, the NATO Innovation Fund, and the European Investment Fund’s defense-equity programs and EU schemes, such as EUDIS.

Then learn the unglamorous lesson from Ukraine: professionalize your financial reporting early. Ukrainian bankers are clear that even with subsidized loans on the table, they don’t see “a queue of clients,” partly because fast-growing defense firms often lack mature management and reporting systems. The banks can’t underwrite, or even onboard, what they can’t read. The founders who get the account and the loan are the ones who can hand a banker clean books. No blindfold required.

What actually needs to change at the policy level

Founder workarounds only go so far. The real fix is structural, and the outline of it is already visible. The EU has started moving. The Defence Readiness Omnibus, adopted in June 2025, and the subsequent Commission Notice (C/2025/4950) and delegated regulation narrowed the toxic, vague category of “controversial weapons” down to “prohibited weapons“: only those actually banned by international conventions are now automatically excluded. That sounds like legal hair-splitting, but it’s the single most important thing Brussels has done here: it drags legitimate dual-use defense companies out of the ESG grey zone and tells banks, in writing, that financing them is allowed. The UK’s FCA said much the same in plain language: nothing in the rules stops finance for defense. The bigger ReArm Europe / Readiness 2030 architecture aims to mobilise up to €800 billion over four years, with the €150 billion SAFE loan instrument and an expanded EIB mandate behind it.

But clarifying the rules isn’t the same as making accounts open and credit flow. Three more things need to happen.

First, fix the onboarding wall. A clarifying notice in Brussels doesn’t reach the compliance algorithm that auto-rejects a drone startup at account opening. Banks need explicit, safe-harbour guidance (and supervisory cover) to onboard vetted defense SMEs without treating “defense” as a red flag in itself.

Second, sovereign guarantees on the compliance and credit risk. The reason a commercial bank won’t touch a defense startup is that it’s pricing reputational and regulatory risk it can’t quantify. Take that risk off the bank’s books and the money moves. Ukraine has already proven the model: its government subsidises defense loans down to 5% interest and covers the spread: a blueprint lifted, charmingly, from a pre-war agricultural support scheme. Over 20 banks, representing more than 70% of Ukraine’s banking sector, now participate. And the Basel treatment of unrated defense SMEs, which Deutsche Bank is warning about, needs a deliberate fix rather than an accidental penalty.

Third, and this is no longer just an idea: a multilateral defense bank is actually being built. The Defence, Security and Resilience Bank (DSRB), conceived by Rob Murray, who also drew up the blueprints for the NATO Innovation Fund and DIANA, is a multilateral institution owned exclusively by nation-states, modelled on the World Bank but dedicated to collective defense and security. Its design answers the exact problem described here. As KPMG, advising on the new architecture, notes, defense-supply-chain SMEs struggle to secure commercial loans because of long lead times and ESG-driven lending criteria; the DSRB is built to fix that by raising money on capital markets through AAA-rated bonds backed by member-state guarantees, then channelling long-term, low-cost loans and guarantees into defense and its supply chain. That structure does three things at once: it relieves national budgets without inflating sovereign debt, it gives suppliers the multi-year financing certainty they need to scale, and it uses guarantees and risk-sharing to draw in private capital that commercial banks will not deploy alone. The economic argument is the clincher: money pushed through ordinary budgets tends to be absorbed by imports, wages and a handful of prime contractors, whereas capital routed through a multilateral lender flows down the entire supply chain, producing more durable growth. The bank is well past the manifesto stage. A coalition of major lenders, among them JPMorgan, ING, Commerzbank and LBBW, alongside all six of Canada’s largest banks, has signed on as partners; it is targeting AAA-rated bonds and an initial balance sheet of around £100 billion; and as of April 2026 Canada has been confirmed as host of its headquarters, with formal establishment through a founding charter ratified by anchor nations expected by the end of 2026. Murray’s framing is hard to argue with: Europe is, functionally, at war, and as he puts it, “this is no different from conflicts that go back centuries,” which have typically been funded through credit. Multilateral development banks were built to finance roads and dams; this is the same instinct, pointed at deterrence, and unlike a private Erebor it is aimed squarely at the sovereign and supply-chain layer.

The bottom line

There’s a uniquely European absurdity in all of this. The continent has decided, correctly and at last, that it must rearm. It has unlocked hundreds of billions in headline spending and minted a generation of defense unicorns. And it has left in place a banking system that still treats the average defense founder like a money-laundering risk: one that makes a Ukrainian CEO blindfold his bankers, forces a NATO-created fund to fight for a checking account, and pushed a US defense founder to charter his own bank rather than keep begging for one.

The good news is that almost everything here is a policy choice, not a law of nature. The Baltics chose to make banking work for defense. France chose it. Brussels has started choosing it. The question for the next two years is whether the rest of Europe, Germany very much included, chooses it fast enough to matter, or whether the funding rounds keep being celebrated while the most basic plumbing leaks. Because in a war, the side that can fund its builders cheaply, quickly, and at scale tends to win. Right now, that’s a competition Europe is choosing to make harder than it needs to be.

Note: This article reflects publicly reported information as of June 2026. It’s commentary, not investment or legal advice.