Space IPOs in 2026: What York Space Systems Tells Us About the Market’s Reopening

Public markets are no longer financing the future of space - they are financing its supply chain.

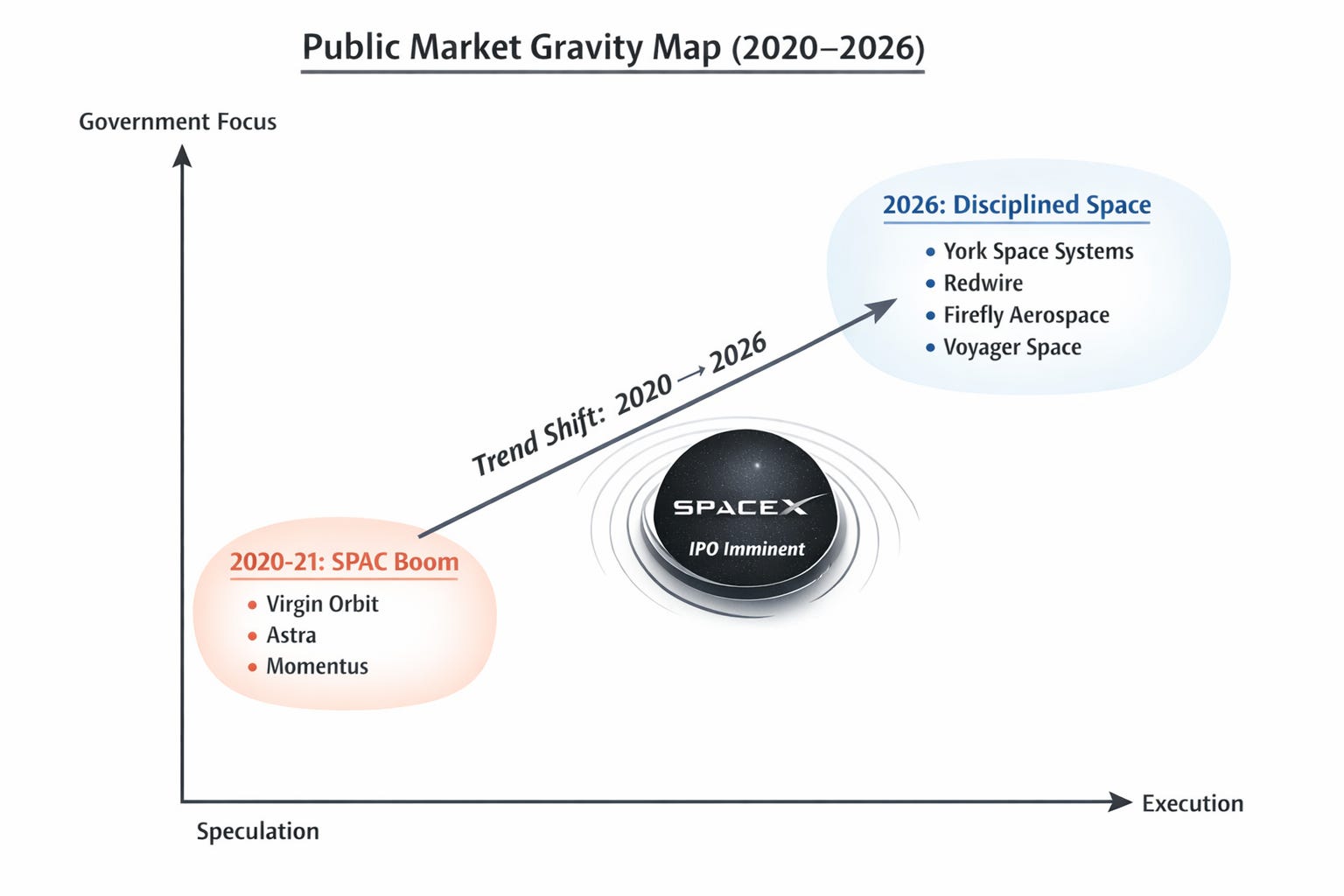

For several years, space companies were effectively locked out of public markets. The speculative excesses of the SPAC era had collapsed under the weight of missed projections, rising rates, and unforgiving balance sheets. By 2023, the window was shut.

In 2026, that window is reopening, but narrowly. This is not a revival of 2021-style exuberance. It is a more disciplined re-entry shaped by operational credibility, government demand, and a renewed intolerance for long-duration promises without near-term execution.

York Space Systems’ $629 million initial public offering is the clearest example so far of what now works. But the deeper story is structural: which space business models can survive public scrutiny, which cannot, and what this says about the next phase of the orbital economy.

A Selective Reopening

York Space Systems went public in on January 29th after increasing the size of its IPO and pricing at the top of its proposed range. The company sold 18.5 million shares at $34 apiece, raising $629 million, an outcome that would have been unremarkable in 2021, but is striking in today’s market.

The contrast matters. From 2022 through much of 2025, space IPOs were either postponed, downsized, or followed by sharp post-listing declines. Investor appetite did not disappear entirely, but it became highly conditional. Scale, revenue visibility, and customer credibility began to matter more than long-term narratives about trillion‑dollar space economies.

York cleared that bar not because it is profitable - it is not - but because it fits the emerging profile of what public investors now tolerate: a company with real missions flown, real contracts signed, and a customer whose ability to pay is not cyclical.

A Brief History of Space IPOs - and the Hangover

The current reopening of the space IPO market only makes sense when set against the boom-and-bust cycle that preceded it.

2020: The Opening Act

The modern wave began just before the pandemic. Virgin Galactic became one of the first pure-play space companies to reach public markets, while early SPAC entrants such as Momentus and HyTech signaled how easily capital could be accessed - even by companies with limited operational maturity.

2021: Peak Space SPACs

The floodgates opened. This was the high-water mark for space listings, dominated almost entirely by SPAC mergers. Rocket Lab, AST SpaceMobile, Astra, BlackSky, Redwire, Spire Global, Arqit, and others all went public during this period. Many promised rapid constellation deployment, launch cadence growth, or vertically integrated space platforms. Valuations were rich, projections aggressive, and due diligence light.

2022: Momentum Breaks

Listings continued into early 2022, most notably Satellogic, but market conditions deteriorated rapidly. Rising interest rates, regulatory scrutiny, and disappointing post-merger performance exposed structural weaknesses across the sector.

2023: The Pause

By 2023, the window had effectively closed. New listings dried up, and failures became impossible to ignore. Virgin Orbit’s bankruptcy crystallized the risks embedded in the earlier cycle and further eroded investor confidence.

2024: Stabilization Without Listings

Public markets steadied, but space companies largely stayed private. Notably, no major U.S. space firms went public via SPAC, even as a handful of listings occurred in Japan and South Korea. The lesson from the prior cycle had been absorbed.

2025: A Tentative Return - On New Terms

When space companies did return to public markets, they did so cautiously and mostly through traditional IPOs. Voyager Technologies, Firefly Aerospace, Karman Holdings, and Astroscale tested investor appetite with more conservative positioning and clearer revenue stories. Performance was mixed, but the era of easy capital was decisively over.

What Has Worked - and What Hasn’t

Out of that correction, a pattern has emerged.

Business models that have underperformed tend to share common traits: heavy dependence on future commercial demand, exposure to launch cadence risk, and narratives built around vertical integration before underlying unit economics were proven.

More resilient companies, by contrast, tend to sit closer to government procurement and infrastructure. Defense-linked satellite manufacturing, ground systems, mission operations, and software that plugs directly into national security architectures have fared better, even when unprofitable, because demand is contractually anchored and politically durable.

This distinction explains why some publicly traded space firms continue to struggle while others retain institutional support despite losses. It also explains why York’s IPO succeeded where many earlier offerings did not.

York Space Systems in Context

Founded in 2012 by CEO Dirk Wallinger, York Space Systems builds and operates satellites primarily for U.S. government customers. As of September 30, 2025, the company had completed 74 missions and logged more than four million hours in orbit- figures that place it well beyond the prototype stage.

Financially, York is growing but unprofitable. Revenue reached $280.9 million in the first nine months of 2025, up from $176.9 million a year earlier. Net losses over the same period totaled $56 million, an improvement from the prior year but still substantial. Management has been explicit that losses are likely to continue for several years and that profitability is uncertain.

What distinguishes York is not its margin profile, but its position in the defense ecosystem. Nearly all of its revenue and backlog are tied to the U.S. Space Development Agency, reflecting Washington’s accelerating investment in proliferated satellite constellations for missile tracking, communications, and resilience in contested orbits.

York also emphasizes cost and speed, claiming its standardized satellite platform can be produced at roughly half the cost of competitors’ systems and deployed on compressed timelines. In a defense environment increasingly oriented toward rapid iteration rather than exquisite hardware, that value proposition resonates.

2026 So Far: Fewer Deals, Clearer Signals

York is not the only space-related company to test public markets in 2026, but it is among the most consequential. What stands out is not the volume of offerings, still low by historical standards, but their character. Deals are larger, more conservatively framed, and explicitly tied to existing revenue rather than future optionality.

This marks a sharp departure from the previous cycle. The space IPO market is no longer rewarding ambition for its own sake. It is pricing survivability, state alignment, and operational credibility.

The Coming Benchmark: SpaceX

Hovering over the entire sector is the anticipated public listing of SpaceX, widely expected by market participants to occur around mid‑2026. If it happens, it will not simply be another IPO - it will be a regime‑setting event that pulls space investing out of its niche and into the core of global capital markets.

At a reported target valuation approaching $1.5 trillion, SpaceX would instantly become a valuation anchor for the entire sector. Companies such as Rocket Lab and AST SpaceMobile, long priced as speculative or structurally risky, could suddenly appear undervalued by comparison. Even the rumor of a SpaceX listing in late 2025 triggered sharp moves in space‑adjacent equities, underscoring how starved public markets are for a true category leader.

Beyond sentiment, a public SpaceX would reshape competition. With $30 - $50 billion in fresh capital, the company could further accelerate development of Starship and Starlink, entrenching its dominance in launch and satellite communications. For firms attempting to match SpaceX’s low‑cost, high‑cadence model directly, the squeeze would intensify.

At the same time, differentiated niches would likely benefit. Earth‑observation companies, in‑orbit servicing providers, mission‑specific satellite manufacturers, and software‑centric space firms stand to gain as the broader space economy expands toward a projected $1.8 trillion by the mid‑2030s. Governments, wary of single‑supplier dependence, are also likely to continue supporting second‑source providers, from Blue Origin in launch to Amazon’s Project Kuiper in communications, regardless of SpaceX’s market power.

Finally, disclosure matters. A SpaceX IPO would, for the first time, provide public benchmarks for revenue, margins, capital intensity, and customer concentration at scale. For other space companies, those numbers would function as both roadmap and warning.

Who Could Be Next

Against that backdrop, a small number of private space companies are frequently cited as potential IPO candidates in 2026 or shortly thereafter.

Sierra Space, developer of the Dream Chaser spaceplane, is often mentioned as a leading contender. Its positioning around cargo transport and future commercial space stations aligns closely with NASA and government demand, and its business profile fits the emerging preference for infrastructure over aspiration.

Axiom Space is another name to watch. The company is developing a private space station and has secured substantial customer contracts, though recent leadership changes and a lower private‑market valuation may delay any public listing until after clearer operational milestones are reached.

Blue Origin remains a wildcard. Jeff Bezos’ aerospace company has not announced IPO plans, but analysts continue to speculate that a public listing could follow SpaceX’s debut, particularly if governments seek to ensure durable competition in launch and orbital services.

What unites these potential candidates is not growth hype, but strategic relevance. Each sits at the intersection of national space policy, long‑term infrastructure, and sustained government support.

The Larger Shift

York Space Systems’ IPO is best understood not as a return to the old space investment narrative, but as evidence of a new one. The space economy that public markets are now willing to finance is narrower, more militarized, and more closely tied to government spending than the one envisioned a decade ago.

This is the space Zeitenwende: fewer moonshots, more procurement; fewer promises, more contracts. York made it through the public-market gate because it fits that world. Others will have to adapt, or wait.