Satellite Propulsion Market to Hit $6 Billion by 2032: What's Driving the Growth?

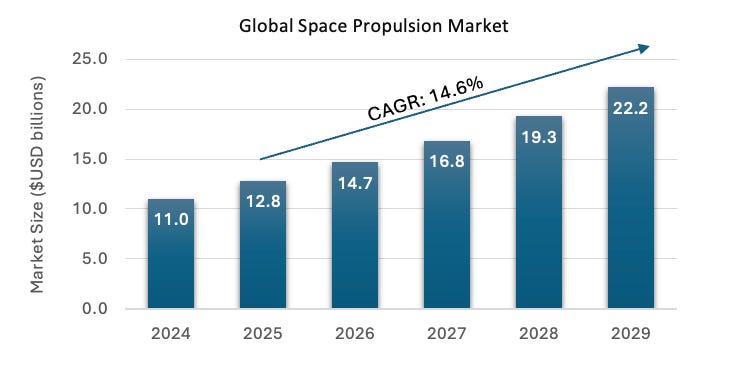

The satellite propulsion market is undergoing a transformative phase, with projections indicating a remarkable growth trajectory from $2.5 billion in 2024 to $6.0 billion by 2032. This expansion is driven by advancements in propulsion technologies, especially electric; the increasing adoption of reusable satellite systems; the surge in satellite launches for commercial, governmental, and scientific applications, especially the rising deployment of small satellite constellations; and increasing investment in space programs. The industry is witnessing a paradigm shift as stakeholders prioritize efficiency, sustainability, and cost-effectiveness in propulsion systems. Electric propulsion systems are at the forefront of this evolution, offering significant advantages in terms of fuel efficiency and extended operational lifetimes, which are critical for modern satellite constellations. This report delves into the key drivers, investment trends, competitive dynamics, and technological innovations shaping the satellite propulsion market.

The Satellite Propulsion Market Landscape

Overview of Market Growth

The satellite propulsion market's projected growth from $2.5 billion in 2024 to $6.0 billion by 2032 represents a compound annual growth rate (CAGR) of approximately 12.2%. This rapid expansion underscores the increasing demand for advanced propulsion systems capable of supporting diverse satellite missions, including telecommunications, Earth observation, navigation, and space exploration.

Electric propulsion systems are emerging as a dominant force within the market due to their superior fuel efficiency and ability to support long-duration missions. These systems reduce propellant mass by up to 90%, enabling lighter satellites and cost-effective operations. Additionally, hybrid propulsion systems that combine electric and chemical technologies are gaining traction for their ability to balance efficiency with responsiveness.

Regional Insights

North America currently leads the satellite propulsion market, accounting for over 42% of global market share in 2024. This dominance is attributed to technological innovation fueled by substantial investments in space exploration programs by NASA and private companies such as SpaceX. The U.S. government's investment in advanced nuclear-powered spacecraft technologies significantly propels the satellite propulsion system market by enhancing civil and military applications,

Europe is also experiencing significant growth, driven by government initiatives like ESA's ARTES program and a strong focus on sustainable propulsion technologies. Meanwhile, Asia-Pacific is emerging as a key player due to China's heavy investments in advanced propulsion systems and Japan's emphasis on green technologies. China in particular is making aggressive investments in satellite propulsion, holding a substantial revenue share in 2024. The growth is attributed to expansion of satellite mega constellations, which require enhanced launch capabilities and innovative propulsion technologies for large-scale deployments.

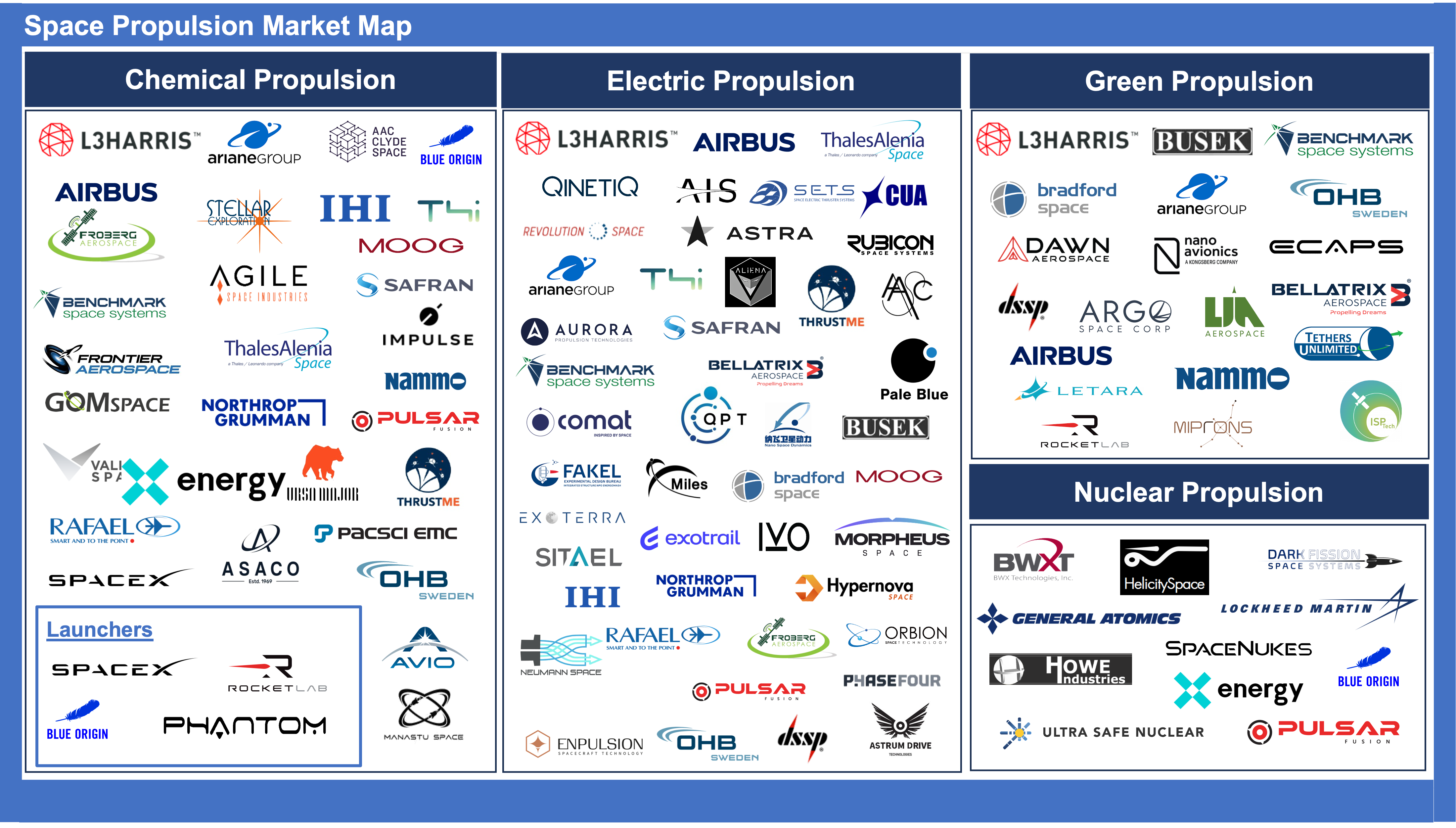

Key Players

The competitive landscape of the satellite propulsion market includes established aerospace giants such as Airbus SE, Thales SA, Northrop Grumman Corporation, and Safran S.A., alongside innovative startups like Dawn Aerospace and Bellatrix Aerospace. These companies are investing heavily in research and development to enhance propulsion efficiency and reduce environmental impact.

Traditional Industry Leaders

Several established aerospace corporations are making significant investments in advanced propulsion technologies:

Northrop Grumman (US) stands as a dominant player in the satellite propulsion market. The company's investments span various propulsion systems utilized in its Pegasus, Minotaur, and Antares rockets, as well as in Delta IV and commercial launch vehicles. Northrop Grumman's extensive international presence and network of offices across Europe, Asia Pacific, and the Middle East have positioned it as a global investment leader in propulsion technologies.

Safran SA (France) continues to be a top investor in the space propulsion sector. The company has consistently allocated substantial resources toward developing cutting-edge propulsion systems, maintaining its position among market leaders through strategic investments in advanced technologies.

Airbus (France) has developed versatile electric thrusters suitable for both geostationary satellites (GEO) and LEO missions. As one of the key players profiled in market analyses, Airbus is investing heavily in adapting to new technologies by focusing on electric and hybrid propulsion systems.

Thales Alenia Space (France) ranks among the top companies driving investment in the satellite propulsion market. The company's consistent appearance in industry analyses demonstrates its commitment to advancing propulsion technologies through significant financial investments.

SpaceX continues to leverage its resources to develop cutting-edge propulsion systems that support ambitious projects such as Starlink's broadband constellation and Starshield's spy satellites network. As a dominant force in the space propulsion system market, SpaceX's investment activities are reshaping industry standards.

Emerging Players and Startups Attracting Significant Funding

Innovative Companies Securing Investment

Alongside established aerospace giants, several specialized propulsion companies and startups are attracting substantial investment:

Phase Four announced the first close of its Series C funding round in early 2025, securing nearly 60% of the target raise with strong participation from new and existing investors. The round is led by Artemis Group Capital, the Oklahoma-based investment firm headed by former NASA Administrator Jim Bridenstine, highlighting growing investor confidence in innovative propulsion solutions.

Kreios Space secured €2.3 million in pre-seed funding for its Air-Breathing Electric Propulsion (ABEP) engine. This funding combines private investments from Grow Venture Partners, XesGalicia, SpaceQuest Ventures, Tasivia Global, and a successful crowdfunding campaign through Startupxplore. The capital will support laboratory testing, new facility construction, and team expansion for their revolutionary fully electric engine that uses only solar energy and atmospheric air as propellant.

Dawn Aerospace is developing green propellant solutions for deep-space missions through partnerships with organizations like DLR. The company specializes in electric and hybrid propulsion systems, focusing on solutions for small satellite propulsion and in-orbit maneuvering.

Drivers of Market Growth

Technological Advancements

Advancements in electric propulsion technologies are revolutionizing the satellite industry. Systems like Hall Effect thrusters and ion thrusters offer high specific impulse (Isp), enabling precise orbital control and extended mission durations. Innovations in materials science, such as carbon fiber composites for lightweight components, further enhance performance metrics while reducing costs.

Moreover, the integration of additive manufacturing techniques allows for the production of complex propulsion components with reduced weight and increased reliability. These technological breakthroughs are expanding the possibilities for satellite missions, from deep-space exploration to low Earth orbit (LEO) constellations.

Cost Efficiency

The plummeting cost of space launches has made satellite deployment more accessible than ever before. Launch costs have decreased from $51,200 per kilogram during the space shuttle era to as low as $100 per kilogram with SpaceX's Starship program. This reduction has shifted focus toward optimizing satellite operations through efficient propulsion systems.

Electric propulsion systems significantly lower operational costs by reducing fuel requirements and extending satellite lifespans. This cost efficiency is particularly beneficial for commercial operators deploying large constellations for telecommunications and broadband services.

Sustainability Goals

Environmental concerns and regulatory pressures are driving the development of eco-friendly propulsion systems that minimize carbon footprints and reduce space debris. Green technologies such as water-based propellants and non-toxic alternatives are gaining traction among operators seeking compliance with regulatory standards.

For example, Japan is investing in mass-production technologies for next-generation green propulsion systems that utilize environmentally friendly propellants. Similarly, Germany's focus on sustainable solutions aligns with global sustainability goals and positions the country as a leader in green aerospace innovation.

Rising Satellite Launches

The exponential increase in satellite launches is a major driver of market growth. The number of satellites launched annually has surged from 500 in 2010 to over 2,000 in 2024. This trend is expected to continue as operators deploy constellations for applications ranging from Earth observation to IoT services.

The demand for efficient propulsion systems capable of supporting these missions is driving innovation across the industry. Electric propulsion systems are particularly well-suited for managing station-keeping and orbital adjustments in densely populated LEO environments.

Investment Trends in Propulsion Technologies

Funding Dynamics

Investment activity within the satellite propulsion sector has intensified as private companies and government agencies recognize its strategic importance. In 2023 alone, HyPrSpace and Leonardo secured funding worth $38 million to develop innovative rocket engines. Similarly, NASA allocated $98 million for solar electric propulsion development as part of its broader commitment to advancing space technology. (NASA, along with the Department of Energy (DOE), is also funding research and development for nuclear thermal propulsion (NTP) systems, with the goal of enabling faster and more efficient deep space exploration, including missions to Mars).

Private sector investments are also on the rise. Companies like SpaceX are leveraging their resources to develop cutting-edge propulsion systems that support ambitious projects, such as Starlink's broadband constellation and Starshield's spy satellites network.

Startup Ecosystem

Startups are playing a pivotal role in driving innovation within the satellite propulsion market. Companies like Dawn Aerospace are developing green propellant solutions for deep-space missions through partnerships with organizations like DLR. Meanwhile, IENAI SPACE secured ESA contracts to advance its ATHENA electric propulsion system. These collaborations highlight the industry's shift toward sustainability and efficiency while fostering technological advancements that benefit both commercial operators and scientific missions.

Strategic Partnerships

Collaborative efforts between government agencies, academia, and private companies are accelerating the deployment of advanced propulsion technologies. For instance, Terran Orbital partnered with Safran Electronics & Defense to explore US-based production of plasma thrusters for satellites. Such partnerships enhance technical expertise while promoting resource sharing across stakeholders.

Competitive Landscape: Traditional vs. Emerging Players

Adaptation Strategies

Traditional aerospace companies are adapting to new technologies by investing in electric and hybrid propulsion systems. For example, Airbus SE has developed versatile electric thrusters suitable for both geostationary satellites (GEO) and LEO missions.

Emerging players like Bellatrix Aerospace are challenging incumbents with innovative solutions tailored for small satellites and CubeSats. These startups leverage their agility to address niche markets while driving competition within the industry.

Market Differentiation

The competitive landscape is characterized by efforts to differentiate products through enhanced capabilities and cost-effectiveness. Companies offering high-performance electric thrusters with superior thrust-to-power ratios gain an edge over competitors relying solely on traditional chemical systems. Additionally, operators prioritizing sustainability can attract environmentally conscious customers seeking compliance with stringent regulations on toxic propellants.

The Future Outlook: Dominant Technologies & Market Opportunities

Electric Propulsion Systems

Electric propulsion systems are poised to dominate the satellite market over the next decade due to their unparalleled fuel efficiency and ability to support long-duration missions. Innovations such as solar electric propulsion (SEP) and multi-modal engines will further enhance their capabilities while addressing challenges related to power consumption.

Hybrid Propulsion Systems

Hybrid systems combining electric efficiency with chemical responsiveness offer promising solutions for missions requiring rapid maneuvers or high delta-V capabilities. These technologies bridge gaps between traditional approaches while catering to evolving mission requirements. Terran Orbital partnered with Safran Electronics & Defense to explore US-based production of plasma thrusters for satellites, demonstrating collaborative investment approaches that enhance technical expertise while promoting resource sharing across stakeholders.

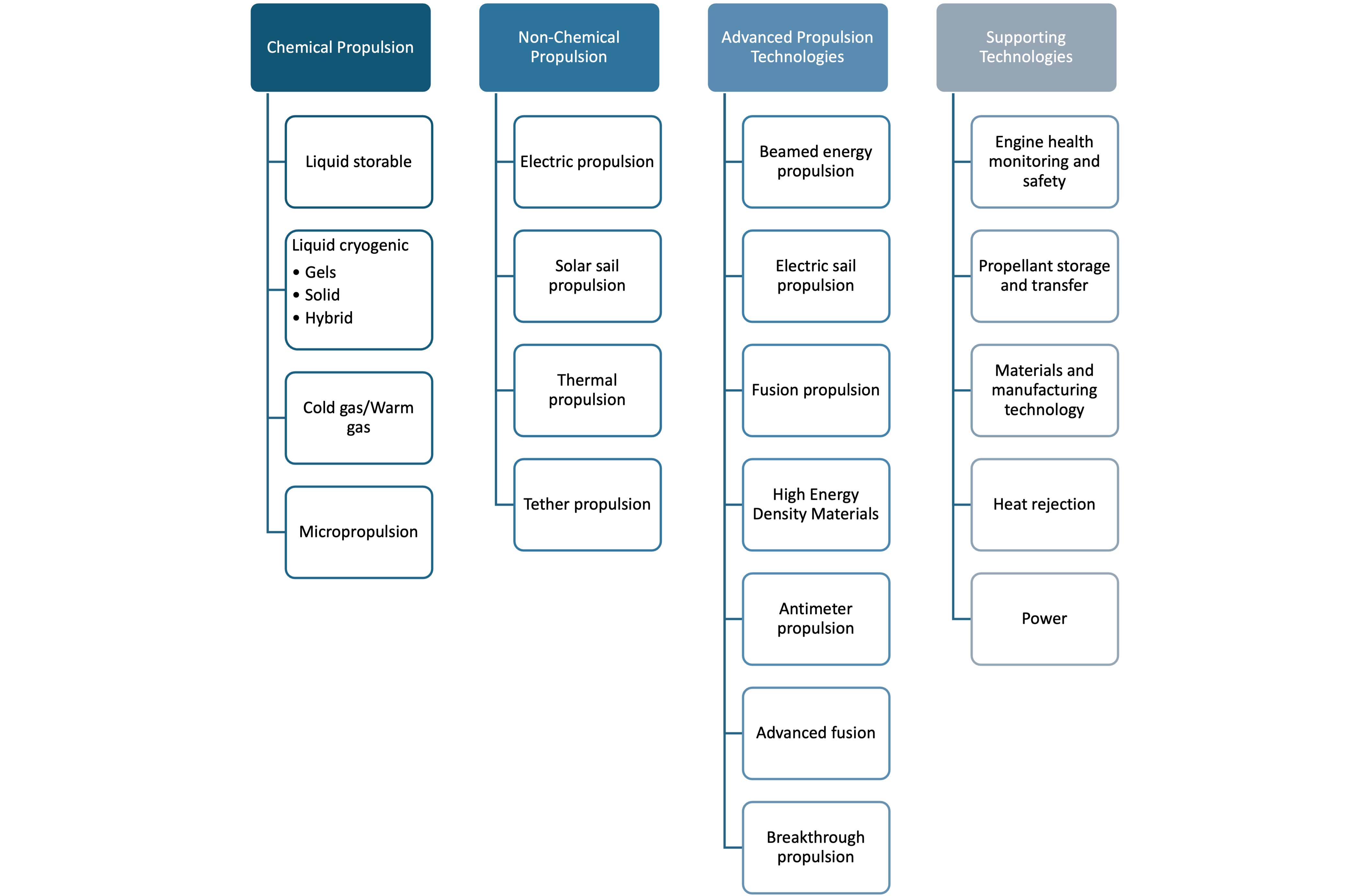

Alternative and Emerging Types of In-Space Propulsion

The development of alternative propulsion systems is driven by sustainability goals and deep-space exploration. Additionally, as the demand for satellite constellations rises, so too does the need for innovative propulsion solutions that can support these missions.

Nuclear thermal propulsion has significant promise for deep space missions as it offers a hybrid approach that combines high efficiency with the potential for crewed missions to Mars or further. In fact, nuclear thermal propulsion systems currently under development by NASA and DARPA promise to reduce Mars transit times by 40% compared to chemical rockets.

Solar sail technology provides a revolutionary approach using solar energy, making it viable for extended missions beyond our solar system without the need for traditional propellant. Solar sails harness the pressure of sunlight to propel spacecraft. While the concept is still being actively researched, it holds promise for cost-effective exploration of distant regions of the solar system.

Fission fragment and plasma propulsion technologies represent advanced concepts currently under exploration. Fission fragment propulsion could theoretically allow for more rapid travel within the solar system, while plasma propulsion utilizes electromagnetic fields to accelerate ionized gas, promising higher speeds for future missions.

Propellant-less systems, which do not require traditional propellants, include photonic propulsion, which uses light pressure from lasers or other directed energy sources, as well as gravity assist, which utilizes the gravity of planets or moons to alter a spacecraft's trajectory.

Types of In-Space Propulsion

Emerging Applications

The growing deployment of small satellites opens new avenues for compact electric thrusters designed specifically for CubeSats or nanosatellites operating within LEO constellations. These applications benefit from reduced launch costs while supporting data-intensive services like broadband internet or Earth observation.

Conclusion: Strategic Insights & Recommendations

The satellite propulsion market's projected growth reflects its critical role in shaping the future of space exploration and communication. As demand for efficient, sustainable, and cost-effective propulsion systems continues to rise, companies leading in investment are focusing on electric propulsion technologies, green propellants, and hybrid systems that balance efficiency with performance.

The competitive landscape features traditional players like Northrop Grumman, Safran SA, and Airbus adapting through strategic investments, alongside emerging companies like Phase Four, Kreios Space, and Dawn Aerospace, securing substantial funding for revolutionary propulsion solutions. This diverse investment ecosystem is driving technological advancement and market growth, positioning satellite propulsion as a critical component of the expanding space economy.