February 2025 Space Stock Review

MARKET COMMENTARY

Public Markets

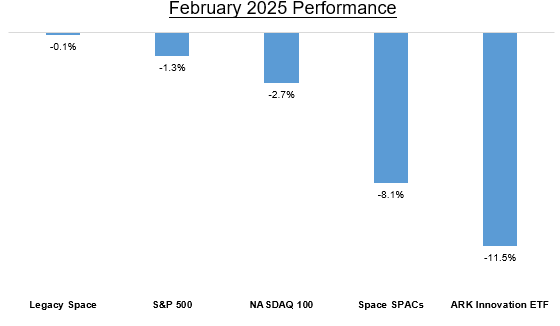

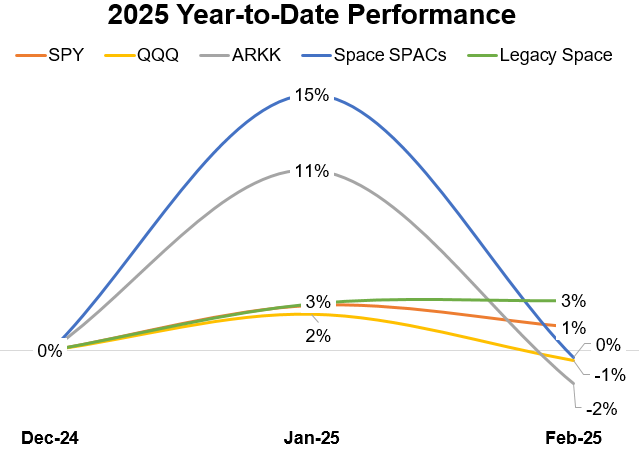

The markets experienced fluctuations in February 2025 due to various risks such as economic slowdown, geopolitics, trade wars, and high valuations, which led to increased stock volatility. Riskier assets like space SPACs and companies held by the ARK Innovation ETF saw a significant correction, erasing gains made in January.

While macroeconomic uncertainty remains at high levels, market uncertainty continues to rise. It appears unlikely that economic and geopolitical uncertainty will be resolved in the near term, suggesting ongoing market volatility is probable.

Private Markets

1. K2 Space (US) raised a $110M Series B (total funding: $176M). The company develops innovative satellite buses, supporting space missions with efficient design and performance across various orbits.

2. Ark Edge Space (Japan) raised a $51.5M Series B (total funding: $74.9M). The company develops advanced micro-satellites, offering a multi-purpose production system for diverse mission portfolios.

3. Karman+ (US) raised a $20M Seed (total funding: $21M). The company is developing an autonomous asteroid mining spacecraft.

4. Magdrive (UK) raised a $10.5M Seed (total funding: $14M). The company is working on high-thrust electric propulsion systems.

5. DPhi Space (Switzerland) raised a $2.3M Pre-Seed (total funding: $2.5M). The company specializes in shared satellites for hosted payloads, simplifying access to space.

6. MESPAC (Italy) raised a €1.5M Seed (total funding: €1.8M). The company provides services for the offshore wind and ocean energy industries, offering accurate, continuous, and spatially refined wind, wave, and environmental data based on Earth Observation technology.

7. Sisir Radar (India) raised a $1.4M Seed (total funding: $1.4M). The company develops synthetic aperture radars, ground-penetrating radars, and hyperspectral imaging solutions.

8. Astrogate Labs (India) raised a $1.3M Seed (total funding: $1.5M). The company enables high-speed satellite communications with laser communication solutions.

9.Urban Sky Theory, Inc. raised aised $30m in Series B funding for its stratospheric Microballoon™s (mHABs), which offer quick, easy, long-duration, and controllable flight in the stratosphere.

SPACE STOCK COMMENTARY

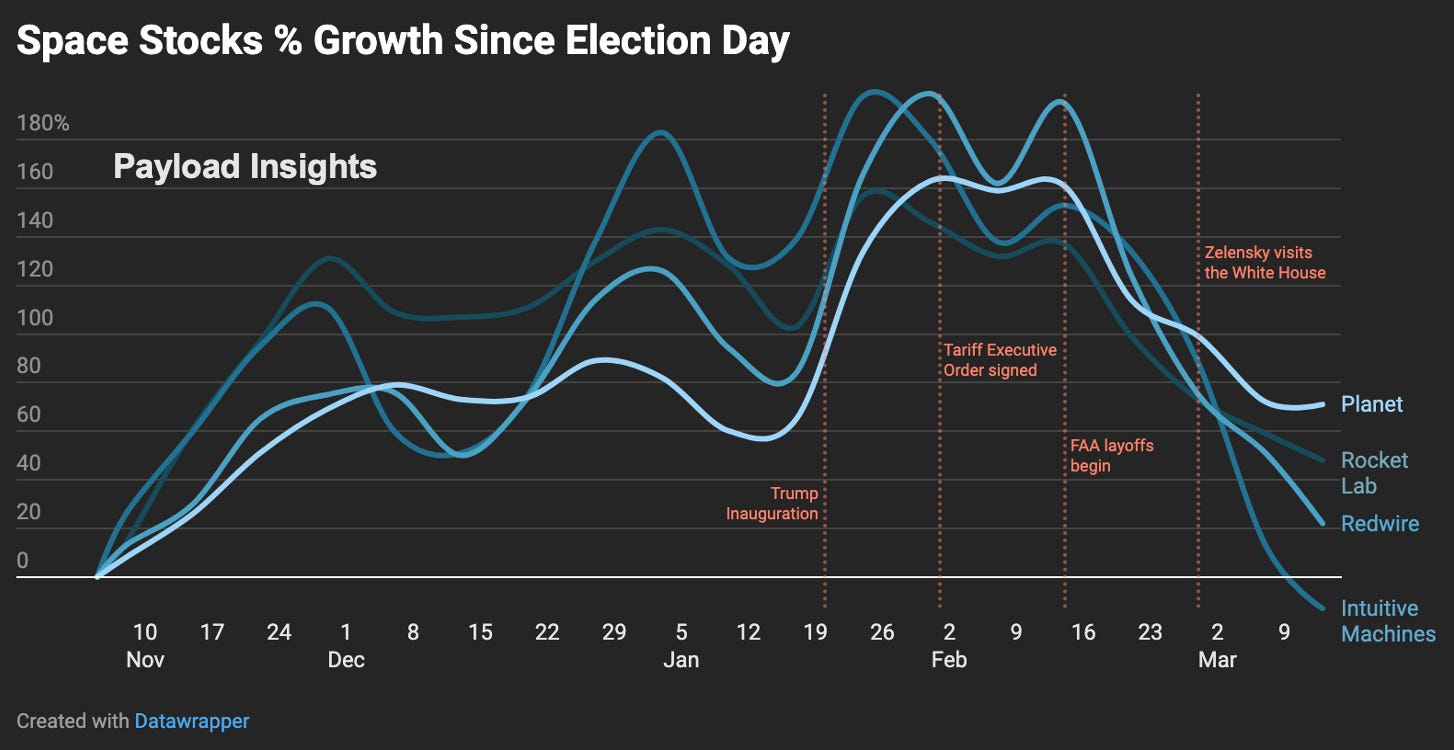

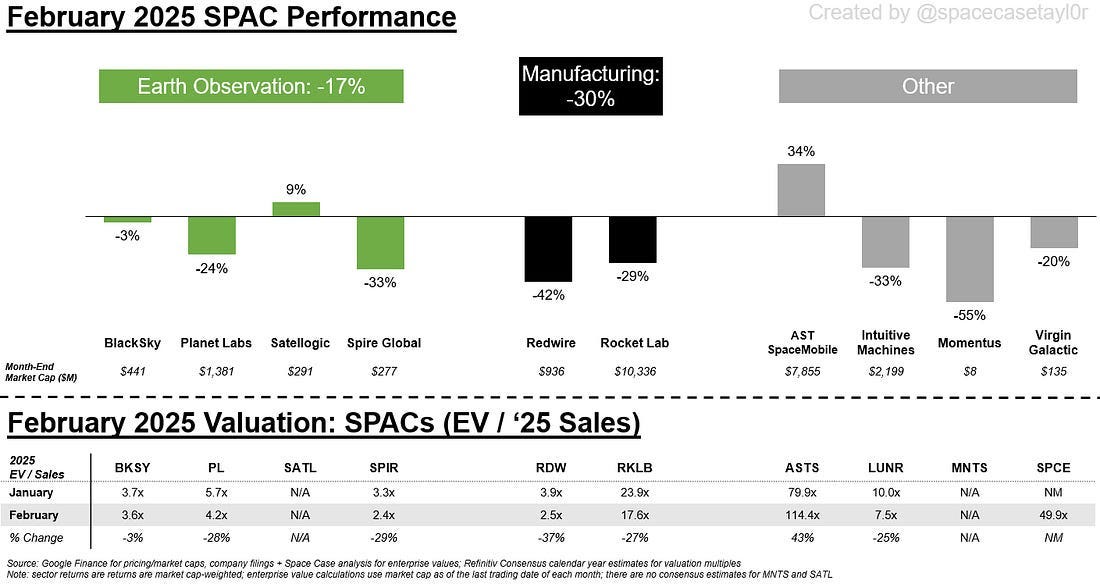

Rocket Lab / RKLB (-29%), Planet Labs / PL (-24%), Redwire / RDW (-42%), and Intuitive Machines / LUNR (-33%) saw January gains wiped out in February but remain above pre-election levels. The decline in these four stocks was expected given their 163% increase after the T2 Admin’s election win in early November through the end of January. News like Planet Labs’ $230M satellite manufacturing deal for SKY Perfect JSAT or Redwire’s acquisition of Edge Autonomy might have justified large stock movements, but the overall negative market shift in February likely caused these stocks to pull back.

Spire Global / SPIR declined -33% in February after disclosing its lawsuit against Belgian analytics provider Kpler for backing out of a $241M acquisition deal.

Spire Global announced plans to sell its maritime business in November 2024, aiming for early 2025 closure. Despite Spire meeting all closing conditions, Kpler refused to close the deal, leading Spire to file a lawsuit with the Delaware Chancery Court on 2/10.

Investors reacted negatively to this news, with SPIR shares dropping -49%. Spire intended to use the transaction proceeds to eliminate debt and invest in growth opportunities; without this cash infusion, Spire faces immediate debt repayment challenges (> $90M due within 12 months from 3Q24) and concerns about its debt management ability due to having only $19.2M cash on hand as of 12/31/2024.

AST SpaceMobile / ASTS increased +34% in February as Direct-to-Cell (D2C) satellite communications (satcom) gained mainstream attention, and the company disclosed its first firm revenue-generating contract.

On 2/9, T-Mobile / TMUS aired a Super Bowl commercial announcing the beta launch of its D2C service in collaboration with Starlink (link to video). This commercial boosted AST SpaceMobile shares by +17% the next day due to heightened interest in D2C services.

T-Mobile's pricing structure aims to drive customers toward premium tiers ($100/mo for one line), making it unlikely that many will pay $15-$20/mo for D2C service regularly.

Consumer D2C service usage is expected to come primarily from customers who receive it "free" via premium plans, basing kickback to D2C providers on actual usage, similar to roaming fees (T-Mobile current roaming fees: $0.10/text, $0.25/min for calls, $2-$5/MB of data).

On 2/26, AST announced a $43M contract from a prime contractor supporting the US Space Development Agency’s (SDA) Proliferated Warfighter Space Architecture (PWSA). This SDA contract is AST’s first firm multi-million dollar agreement, distinct from previous technology readiness-based contracts. The contract language indicates the $43M is unrelated to SDA’s HALO program where AST competes directly for prototype orders.

The government market for D2C services is more compelling than consumer opportunities, as government agencies require reliable remote communication which legacy satcom services provide, but often require bulky and expensive hardware. Consumers may view complete network availability as optional, whereas government customers consider it mission-critical.

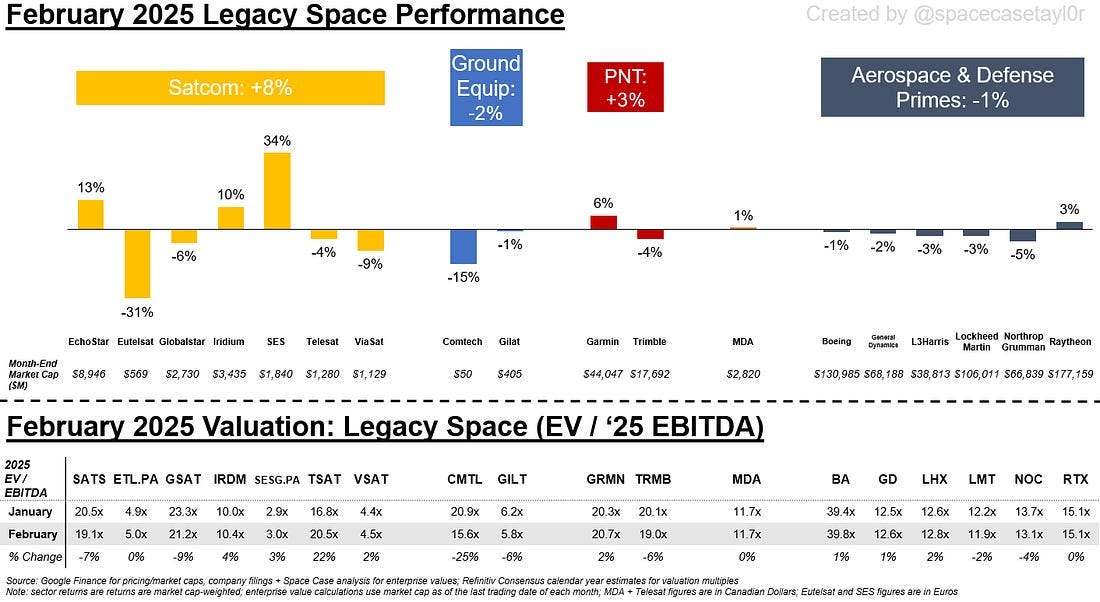

Eutelsat / ETL.PA decreased -31% in February after an unusual earnings announcement.

Eutelsat reported fiscal 1H25 results on 2/14, in line with expectations, but four board members resigned, and the chairman retired, resulting in a -19% share drop and continued decline throughout February.

SES / SESG.PA increased +34% in February due to speculation around C-band spectrum sales and strong 4Q earnings relative to guidance.

The FCC considered changing usage of upper C-band spectrum owned by SES and Eutelsat (link). SESG.PA shares rose +11% following this news, with analysts estimating potential proceeds exceeding $2.9B if auctioned similarly to prior C-band sales.

On 2/26, SES beat 4Q24 earnings guidance, highlighting new C-band sale potential and reaffirming merger plans with Intelsat despite Moody’s downgrade of SES’ outlook to negative on 2/18.